You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

*Official* BBCWatcher club

- Thread starter theokcoral

- Start date

More options

Who Replied?Hi BBCWatcher,

Able to seek some advice from you on my insurance coverage

- 29f/non-smoker (only daughter to 2 elderly parents)

- Great Eastern Supreme Protect Plus 20 : 100k Death/TPD, 100k CI (premium $2.5k/yr for 20 years)

- Great Eastern FlexiLife Early Multiplier 20 : 70k* Death/TPD, 70k* CI, 70k ECI rider, 100k Accident (*300% multiplier till age 65) ($3.2k/yr for 20 years)

- Great Eastern SupremeHealth + Total Health Rider

1) Was chatting with some IFAs and it seems that they are of view that I am overpaying for the coverage that I am getting (as compared to Manulife / Aviva which is more price competitive). Would like to hear your thoughts on this.

2) On coverage, I am keen on increasing coverage for my CI and ECI. With my age, open to explore both whole life / term. Do you have any recommendations on this?

Thanks in advance!

Able to seek some advice from you on my insurance coverage

- 29f/non-smoker (only daughter to 2 elderly parents)

- Great Eastern Supreme Protect Plus 20 : 100k Death/TPD, 100k CI (premium $2.5k/yr for 20 years)

- Great Eastern FlexiLife Early Multiplier 20 : 70k* Death/TPD, 70k* CI, 70k ECI rider, 100k Accident (*300% multiplier till age 65) ($3.2k/yr for 20 years)

- Great Eastern SupremeHealth + Total Health Rider

1) Was chatting with some IFAs and it seems that they are of view that I am overpaying for the coverage that I am getting (as compared to Manulife / Aviva which is more price competitive). Would like to hear your thoughts on this.

2) On coverage, I am keen on increasing coverage for my CI and ECI. With my age, open to explore both whole life / term. Do you have any recommendations on this?

Thanks in advance!

celtosaxon

Senior Member

- Joined

- Oct 4, 2018

- Messages

- 1,748

- Reaction score

- 838

BBC,

I’ve got my first statement from UOBKH for the S27 transaction with SRS. Looks like they first have a debit transaction for S27 purchase which is then offset 2 days later with a credit transaction (cash from SRS), and the ending balance is zero. Am I right to say that for FBAR purposes, this account is reported as $0 highest balance for the year?

UOBKH also forced me to open a CDP account as a backup in case anything goes awry with SRS funding. So it seems like yet another $0 account to report. I just love it.

I’ve got my first statement from UOBKH for the S27 transaction with SRS. Looks like they first have a debit transaction for S27 purchase which is then offset 2 days later with a credit transaction (cash from SRS), and the ending balance is zero. Am I right to say that for FBAR purposes, this account is reported as $0 highest balance for the year?

UOBKH also forced me to open a CDP account as a backup in case anything goes awry with SRS funding. So it seems like yet another $0 account to report. I just love it.

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

It doesn't hurt to shop around.1) Was chatting with some IFAs and it seems that they are of view that I am overpaying for the coverage that I am getting (as compared to Manulife / Aviva which is more price competitive). Would like to hear your thoughts on this.

You seem to be missing the single most important insurance coverage in your situation: Disability Income Insurance. And do you even need life insurance? (Are your elderly parents your dependents?)2) On coverage, I am keen on increasing coverage for my CI and ECI. With my age, open to explore both whole life / term. Do you have any recommendations on this?

I'm not a fan of whole life policies. I highly prefer "Buy Term, (Prudently, Diligently) Invest the Rest" (BTIR).

No. Highest balance means highest balance, and (unfortunately) UOBKH isn't UOB (not really), even assuming your SRS account is with UOB. (It could be with OCBC or DBS.)I’ve got my first statement from UOBKH for the S27 transaction with SRS. Looks like they first have a debit transaction for S27 purchase which is then offset 2 days later with a credit transaction (cash from SRS), and the ending balance is zero. Am I right to say that for FBAR purposes, this account is reported as $0 highest balance for the year?

FinCEN Form 114 isn't something to mess around with. There's zero upside to obfuscation. Just report the two accounts, and report their highest balances.

There are occasions when subaccounts can be rolled up into one line item for reporting. For example, I think you'd probably be on safe grounds if you have an ordinary DBS/POSB bank account and a POSB Invest-Saver account, and rolled those two up into the master account number with the total combined highest balance. That's the same institution, and the accounts are linked. This is really just a hypothetical, though, because POSB Invest-Saver probably doesn't allow U.S. citizens to participate -- and they wouldn't want to anyway since the POSB Invest-Saver funds are "tax toxic."

Yes, but it's handy if you ever want a Singapore Savings Bond or other Singapore Government Security.UOBKH also forced me to open a CDP account as a backup in case anything goes awry with SRS funding. So it seems like yet another $0 account to report. I just love it.

Sweetangtang

Junior Member

- Joined

- Jun 6, 2020

- Messages

- 50

- Reaction score

- 0

It's decent via a zero fee platform, but costs seem to be a little lower via the popular Irish domiciled/London listed funds. At $200/month you could do something like buy $1,200 semiannually via Standard Chartered.

Hi BBC, I saw this on FSM LIONGLOBAL NEW WEALTH SERIES - LIONGLOBAL ALL SEASONS FUND (GROWTH) CL ACC SGD. Is this the same fund? It's in SGD denominations. The expense ratio seems high. May I ask why do you recommend to buy it via SC? Is it recommended to use SRS to buy? Thanks!

celtosaxon

Senior Member

- Joined

- Oct 4, 2018

- Messages

- 1,748

- Reaction score

- 838

No. Highest balance means highest balance, and (unfortunately) UOBKH isn't UOB (not really), even assuming your SRS account is with UOB. (It could be with OCBC or DBS.)

FinCEN Form 114 isn't something to mess around with. There's zero upside to obfuscation. Just report the two accounts, and report their highest balances.

Technically, even a prepaid card can be a reportable account depending on the issuer. Even a foreign credit card that has a credit balance at anytime during the year is reportable! There was a court case that upheld this view, but in that case, the person was clearly trying to get around the system - so I believe that is what drove the ruling.

It is a real minefield out there for US persons... honestly, if they really wanted to, with enough digging they could probably find ‘something’ on just about every US person who lives abroad. I would hate to think they are that mean, especially for people who are genuinely not trying to obfuscate anything and can show reasonable due diligence.

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

The fund Arcaninx referred to? Yes, I think so.Hi BBC, I saw this on FSM LIONGLOBAL NEW WEALTH SERIES - LIONGLOBAL ALL SEASONS FUND (GROWTH) CL ACC SGD. Is this the same fund?

I don't think that fund is a particularly good buy. For SRS funds it can make a little more sense.It's in SGD denominations. The expense ratio seems high. May I ask why do you recommend to buy it via SC? Is it recommended to use SRS to buy?

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

Sure. I'd say the #1 basic investment/financial rule is to avoid everything that could be a "Passive Foreign Investment Company" (PFIC), as the U.S. Internal Revenue Service defines it. Here are examples of PFICs:I'm a 26 year old U.S. Person / Singapore PR that's been living in Singapore for most of my life. I'm looking to start insuring/investing but I'm very wary of the U.S. tax implications and what platforms even allow investing as a non-resident (I was looking into Schwab but my understanding is that things have been getting stricter lately).

I've read a ton of websites but still feel extremely lost. If you could give me some suggestions on what's the best way I can start, you would be doing me a huge favor!

* non-U.S. domiciled funds (such as the LionGlobal's unit trusts, ES3, G3B, MBH, A35, IWDA, VWRA -- basically all the funds that frequently get mentioned in this forum; they're not for you)

* non-U.S. domiciled trusts (such as Ascendas REIT and other non-U.S. REITs)

* non-U.S. listed stocks that aren't nearly "pure plays" (most of the SGX listed stocks, for example)

PFICs are really nasty from a U.S. tax point of view. But that still leaves plenty of choices on the table -- and preferential access to U.S. listed securities.

You'll sometimes run into financial firms that refuse to do business with you. That's generally OK, because what they're peddling is often a PFIC. But there isn't perfect overlap here, so just be a little careful.

There are several U.S. brokers that have no trouble at all accepting U.S. citizens who happen to reside outside the United States as clients. Examples include Interactive Brokers, Firstrade, Zacks Trade, TD Ameritrade, and possibly Schwab. Schwab is awesome if you can manage to get an account open with them, especially if you're just starting out. (It'll require a phone call, though. "Hello, I'm a U.S. citizen living in Singapore, and I'd like to open a Schwab account, please." Can't hurt to try.) If you do manage it then you can just invest in SWYNX every month, the super low cost and super convenient Schwab Target 2060 Index Fund. You'd use FAST to send any number of Singapore dollars to Schwab's local bank account in Singapore in order to deposit funds into your Schwab account (preferably regular, steady savings every month), and Schwab converts them automatically into U.S. dollars at a fairly reasonable cost. Then you just buy SWYNX every month, and since it's US$1 minimum and US$1 per additional purchase, that's easy. (If Schwab opens an account for you they might want something like US$1,000 minimum to open, but after that no minimum.)

What sort of monthly savings flow are you thinking of?

As a Singapore Permanent Resident presumably you'll have some Central Provident Fund contributions. That's fine, even better than fine, but just bear in mind that CPF interest just like other interest is U.S. taxable as it's earned, every year. (Sorry!) Also, your employer's share of CPF contributions counts as U.S. taxable income. There's something called the Foreign Earned Income Exclusion (Form 2555) which you may already be familiar with as part of your U.S. tax returns. (You know what those are, right?) Apparently the employer's share of CPF contributions cannot be excluded from U.S. taxable income using Form 2555. But that's not necessarily a bad thing because it means you could probably open and contribute to a U.S. Roth IRA, which is a U.S. tax advantaged retirement account. Income you're able to shield from U.S. income tax using Form 2555 cannot count as income for purposes of qualifying for an IRA contribution.

Oh, by the way, did you get your US$1,200 in free COVID-19 money, with more possible if Congress and the President come to an agreement? You should be eligible, assuming your income wasn't too high last year.

If you haven't got any U.S. bank or U.S. credit union account, then leading a full financial life can be a little more difficult than it should be. (Example: that US$1,200 in free money from the IRS.) Do you have a low/zero cost U.S. bank or U.S. credit union account yet?

Non-U.S. financial accounts are reportable every year via a particular online form: FinCEN Form 114. You're exempt if your total non-U.S. financial accounts total less than US$10,000. Otherwise, it's easy to fill in. If you get well up into the 6 digits then there's another form (IRS Form 8938) that you'll also need to file. (No, it doesn't make sense that there are two separate forms asking for substantially the same information. Some day that'll probably get fixed.)

You are almost certainly able to vote in the United States. You would vote in your last place of U.S. residence. Alternatively, if you were not born in the United States and never lived in the United States, most states allow you to vote at your U.S. citizen parent's last place of U.S. residence. (If both your parents are/were U.S. citizens, you never lived in the U.S., and they have different last places of U.S. residence -- or maybe one or both currently live in the U.S. -- then you can choose either parent's residence as your voting residence.) If you need help getting this stuff sorted just visit https://www.fvap.gov or https://www.votefromabroad.org (both work; use whichever you find easier to use). The U.S. presidential election is coming up very soon (81 days!), so please get registered RIGHT NOW if you haven't registered yet for 2020. If your U.S. voting place allows online registration in some form, do it that way. (If you never resided in the U.S., please post a follow up since there's a little more detail I need to explain.)

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

BBCWatcher's Favorite Integrated Shield Plans

Updated February 19, 2025

These suggestions are mainly of interest to those of you who are signing up for brand new Integrated Shield plans. I do not generally recommend switching Integrated Shield carriers or "upgrading" plans because you would be subject to a preexisting condition reset and possibly a new congenital abnormalities waiting period. These are my personal views only. Do your own due diligence, please!

Private hospital plan, wide network

I really don’t like this segment of the market, and I like it even less with the MOH's new cancer drug coverage rules that eliminate "as charged" coverage. So I don't have a strong recommendation in this category. I think I'd pick between Great Eastern and Prudential. Of course I'd only buy the lowest cost rider.

I used to have a clear favorite in this segment: AIA. But I'm quite disappointed with how AIA is handling the MOH's new cancer drug coverage rules (a separate rider). If AIA fixes these issues then AIA will probably be my favorite again in my least favorite segment.

Private hospital plan, narrow network

Raffles Shield A + Raffles Hospital Option + Key Rider. This plan combination costs less than every other private hospital Integrated Shield plan, but your private hospital network consists of just one hospital: Raffles Hospital. I suggest you stay in a 4 bedded ward at Raffles Hospital just to be careful managing costs against this plan’s lower annual limit. However, this plan's cancer coverage isn't great after the MOH-mandated rule changes.

Prudential's PRUShield Plus (plus lowest cost rider) is a public hospital A ward plan, but it covers planned medical care at Regency Specialist Hospital in Johor with a referral from HMI Medical in Singapore. Since Regency Specialist Hospital is a private hospital PRUShield Plus's private hospital proration factor (65% as I write this) will apply. However, since the cost of care at Regency Specialist Hospital is substantially lower than what a private hospital in Singapore would charge the out-of-pocket cost should be lower. MediSave dollars can be used at Regency Specialist Hospital.

Public hospital A ward plan

If you're going to go riderless I like Singlife since they cap co-insurance per policy year even without a rider. The annual co-insurance cap is $25,500 which dovetails nicely with many employer-provided medical insurance benefits. Cancer drug coverage is quite limited, though, as a result of the 2023+ MOH rule changes. Singlife offers a standalone cancer treatment policy available to both Singlife and non-Singlife Integrated Shield policyholders.

If you're going to buy a rider and/or are concerned about the cancer drug coverage part I'd go with Prudential or Great Eastern, in both cases with their lowest cost rider.

Foreigners can buy a few plans in this segment (including Prudential's PRUShield Plus) but not in the next segment I’m about to describe. So if you’re a foreigner, here’s where you stop.

”As charged” public hospital B1 ward plan

This segment of the market is what I consider a genuine insurance necessity (for Permanent Residents certainly; often for citizens too), whereas all the above segments dip into the non-necessity/luxury areas at least a bit.

For Singaporean citizens I prefer Great Eastern in this segment because the cancer drug coverage is much better than Singlife's, the runner up in my view. Great Eastern's organ transplant coverage is a little better, too. It looks like Singlife is better for community hospital coverage and final expenses, as examples. (Plus the now market leading $25,500 co-pay cap in the riderless base plan.) Just look at the benefit schedules to compare.

The problem for PRs is that most Integrated Shield plans in this segment charge PRs the same premiums but apply a proration factor to reduce coverage. I really wish they'd instead charge PRs slightly higher premiums and eliminate the proration factors (except for A ward and private hospital proration factors). Income Insurance is one of the few exceptions (only exception?), but in my view their public hospital B1 plan/rider is merely average. If you're a PR and don't mind spending a little extra, take a look at the public hospital A ward plans.

Updated February 19, 2025

These suggestions are mainly of interest to those of you who are signing up for brand new Integrated Shield plans. I do not generally recommend switching Integrated Shield carriers or "upgrading" plans because you would be subject to a preexisting condition reset and possibly a new congenital abnormalities waiting period. These are my personal views only. Do your own due diligence, please!

Private hospital plan, wide network

I really don’t like this segment of the market, and I like it even less with the MOH's new cancer drug coverage rules that eliminate "as charged" coverage. So I don't have a strong recommendation in this category. I think I'd pick between Great Eastern and Prudential. Of course I'd only buy the lowest cost rider.

I used to have a clear favorite in this segment: AIA. But I'm quite disappointed with how AIA is handling the MOH's new cancer drug coverage rules (a separate rider). If AIA fixes these issues then AIA will probably be my favorite again in my least favorite segment.

Private hospital plan, narrow network

Raffles Shield A + Raffles Hospital Option + Key Rider. This plan combination costs less than every other private hospital Integrated Shield plan, but your private hospital network consists of just one hospital: Raffles Hospital. I suggest you stay in a 4 bedded ward at Raffles Hospital just to be careful managing costs against this plan’s lower annual limit. However, this plan's cancer coverage isn't great after the MOH-mandated rule changes.

Prudential's PRUShield Plus (plus lowest cost rider) is a public hospital A ward plan, but it covers planned medical care at Regency Specialist Hospital in Johor with a referral from HMI Medical in Singapore. Since Regency Specialist Hospital is a private hospital PRUShield Plus's private hospital proration factor (65% as I write this) will apply. However, since the cost of care at Regency Specialist Hospital is substantially lower than what a private hospital in Singapore would charge the out-of-pocket cost should be lower. MediSave dollars can be used at Regency Specialist Hospital.

Public hospital A ward plan

If you're going to go riderless I like Singlife since they cap co-insurance per policy year even without a rider. The annual co-insurance cap is $25,500 which dovetails nicely with many employer-provided medical insurance benefits. Cancer drug coverage is quite limited, though, as a result of the 2023+ MOH rule changes. Singlife offers a standalone cancer treatment policy available to both Singlife and non-Singlife Integrated Shield policyholders.

If you're going to buy a rider and/or are concerned about the cancer drug coverage part I'd go with Prudential or Great Eastern, in both cases with their lowest cost rider.

Foreigners can buy a few plans in this segment (including Prudential's PRUShield Plus) but not in the next segment I’m about to describe. So if you’re a foreigner, here’s where you stop.

”As charged” public hospital B1 ward plan

This segment of the market is what I consider a genuine insurance necessity (for Permanent Residents certainly; often for citizens too), whereas all the above segments dip into the non-necessity/luxury areas at least a bit.

For Singaporean citizens I prefer Great Eastern in this segment because the cancer drug coverage is much better than Singlife's, the runner up in my view. Great Eastern's organ transplant coverage is a little better, too. It looks like Singlife is better for community hospital coverage and final expenses, as examples. (Plus the now market leading $25,500 co-pay cap in the riderless base plan.) Just look at the benefit schedules to compare.

The problem for PRs is that most Integrated Shield plans in this segment charge PRs the same premiums but apply a proration factor to reduce coverage. I really wish they'd instead charge PRs slightly higher premiums and eliminate the proration factors (except for A ward and private hospital proration factors). Income Insurance is one of the few exceptions (only exception?), but in my view their public hospital B1 plan/rider is merely average. If you're a PR and don't mind spending a little extra, take a look at the public hospital A ward plans.

Last edited:

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

SWYNX is Schwab’s 2060 target date index fund. It’s a single fund that does everything a regular saver needs for a primarily U.S. dollar-oriented retirement in approximately 2060 (since the bond component is in U.S. dollars). If you don’t actually end up retiring in a U.S. dollar-oriented country then you can make some adjustments many, many years from now, but this is a good, simple choice right now for long-term investing (U.S. person).I'll give Schwab a call tomorrow and see if I can open an account! What's the reason that you recommend SWYNX? (I'm not really aware of the alternatives)

Yes.By monthly savings flow, do you mean how much am I looking to set aside every month for investing?

You’re allowed to if you have (a) earned income (such as the employer’s CPF contribution) (b) that hasn’t been excluded via Form 2555 (c) don’t exceed the income limit for contributing directly to a Roth IRA and (d) don’t exceed the annual contribution limit or your unexcluded earned income, whichever is lower. [If you violate requirement (c) then congratulations, and there’s a workaround available. Ask if you’d like to know more.] A Roth IRA means that you contribute after tax dollars to a specific account — into a Schwab IRA, for example — and then the funds are completely U.S. tax free if you only withdraw them at age 59 1/2 or later (earlier in a few narrow cases). There’s no requirement to withdraw them, however. No U.S. dividend, interest, or capital gains tax! Awesome, right? However, if you withdraw dollars too early, you pay ordinary taxes plus a small (but non-zero) tax penalty. You can make any investments that the IRA custodian allows (such as a low cost U.S. domiciled stock index fund), you can change your mind about the investments, and you can move your IRA to another IRA custodian if you happen not to like the one you’ve got.I'm generally familiar with Form 2555 but I have not considered opening a Roth IRA alongside CPF, is that something you recommend?

Anyway, yes, I’d recommend a Roth IRA if you’re eligible. It’s the first stop in retirement savings because of the tax advantages. And in some cases the tax advantages are internationally respected since the U.S. has tax treaties that honor the Roth IRA in some cases. In other cases, like Singapore, there are no local taxes on such investments, so it still works great.

Yes, maybe. Alliant Credit Union may be willing to open an account for you, and they’re terrific. Their ATM/debit card is truly awesome, although so is Schwab’s. PenFed and the State Department Federal Credit Union are also known to be pretty friendly to U.S. expats. If you’ve got a U.S. mailing address — a trusted friend’s or family member’s for example — then you should be able to open an American Express Bluebird account at Bluebird.com using that address plus your U.S. Social Security Number (which they definitely require). Using a VPN is probably a good idea, too. Bluebird is a basic consumer bank account, and it’s mostly fee free. The few fees they’ve got should be easily avoidable. They provide an American Express debit card which is pretty decent, actually.I do not have a U.S. bank account as I came here at a young age, is there a way to open one without flying back?

How young, if you don’t mind my asking?

Correct. May I ask which state?I was born in the U.S. and resided in the same place of residence until my family emigrated to Singapore, so it sounds like I should be registering to vote using that address.

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

The United States, other countries that use the U.S. dollar (example: El Salvador), and countries with currencies firmly pegged to the U.S. dollar (example: Kuwait).What is considered a U.S. dollar-oriented country?

OK. Just be aware of what citizenship(s) your child(ren) will or will not be eligible for at birth, and depending on the other parent and per U.S. and other nationality laws. It’s really, really tough to be born stateless in this world. In most cases you won’t be able to pass U.S. citizenship to a child born outside the United States since you haven’t lived in the U.S. for at least 5 years, at least 2 of which were after age 14. (Children born inside the U.S., including its airspace and territorial waters, are born U.S. citizens — except the children of foreign diplomats.)I came from Arizona around the age of 3, so it's been a while!

Arizona is a super competitive state in the upcoming election. Register and request a ballot now!

Check this page. Once you get a U.S. bank or U.S. credit union account try the “Get My Payment” button and see if that works, or the other button if applicable. You’ll need your U.S. account’s “routing number“ and account number. For example, Alliant Credit Union’s routing number is 271081528.I tried googling information about this but I must not be using the correct search terms, how do I check if I'm eligible?

Last edited:

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

The most important rider? Because if you need life insurance (the base plan), you need disability income insurance even more. (You may also need DII even if you don’t need life insurance.) Whether you get that specific DII rider or another policy is a separate question.Hi BBC, why is the dii rider in the saf aviva plan the most important in your opinion?

bladez87

Arch-Supremacy Member

- Joined

- Dec 13, 2008

- Messages

- 22,513

- Reaction score

- 1,228

Doesn't the ci or tpd rider provide similar use case as the dii?The most important rider? Because if you need life insurance (the base plan), you need disability income insurance even more. (You may also need DII even if you don’t need life insurance.) Whether you get that specific DII rider or another policy is a separate question.

Sent from Xiaomi POCO F2 PRO using GAGT

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

Certainly not.Doesn't the ci or tpd rider provide similar use case as the dii?

fujitsu555

Member

- Joined

- Sep 27, 2007

- Messages

- 103

- Reaction score

- 0

Whole life insurance (with CI & ECI) for young children

Hi Bbcwatcher, what's your view on getting whole life insurance (with CI & ECI) for young children (below 5)? Do you think it is good to lock in their insurability with a lower premium by buying early?

Hi Bbcwatcher, what's your view on getting whole life insurance (with CI & ECI) for young children (below 5)? Do you think it is good to lock in their insurability with a lower premium by buying early?

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

No, I don't think it's a good idea.Hi Bbcwatcher, what's your view on getting whole life insurance (with CI & ECI) for young children (below 5)? Do you think it is good to lock in their insurability with a lower premium by buying early?

5408854088

High Supremacy Member

- Joined

- Apr 3, 2007

- Messages

- 32,006

- Reaction score

- 29

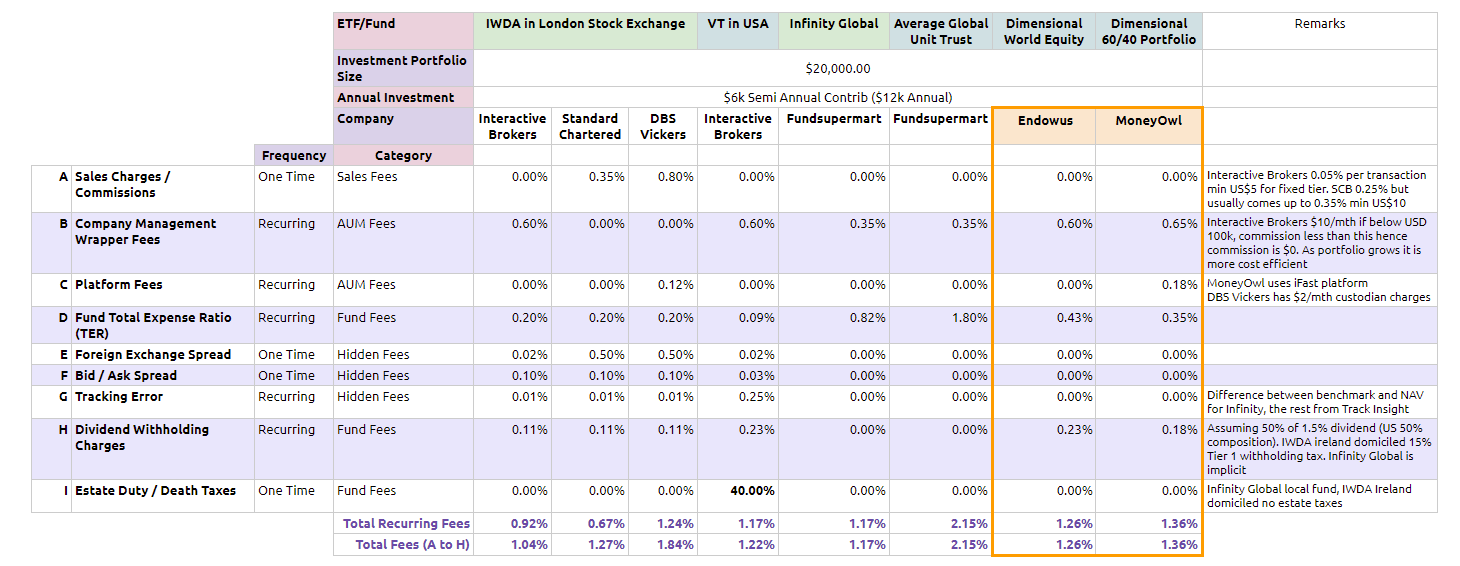

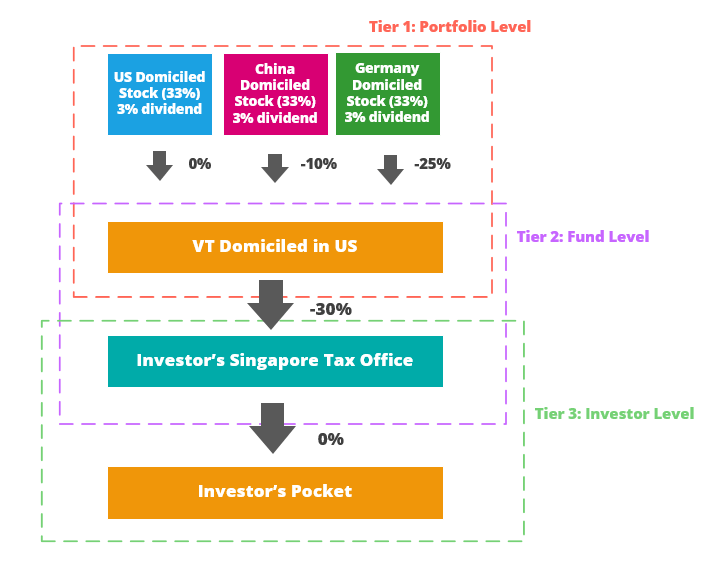

this article compares VT, IWDA, and DFA World Equity Fund. any thoughts?

VT has lower expense ratio, forex risk, 30% dividend withholding tax, estate tax, dividend distributing, brokerage fees.

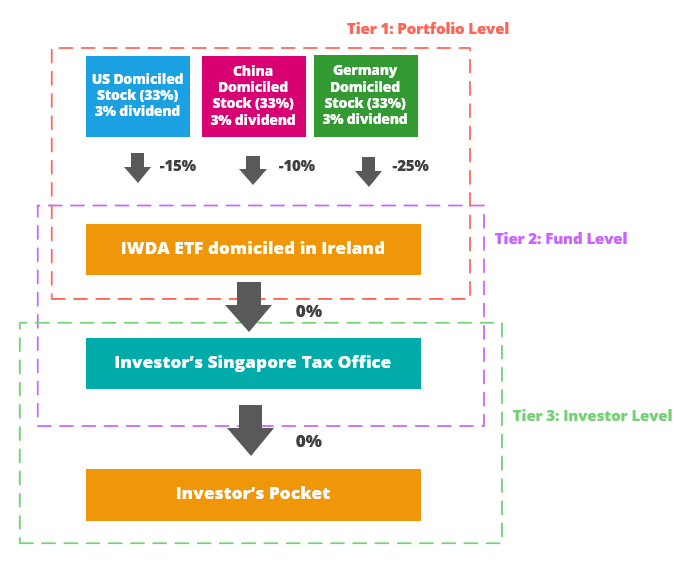

IWDA has lower expense ratio, forex risk, 15% dividend withholding tax, no estate tax, dividend accumulating, brokerage fees.

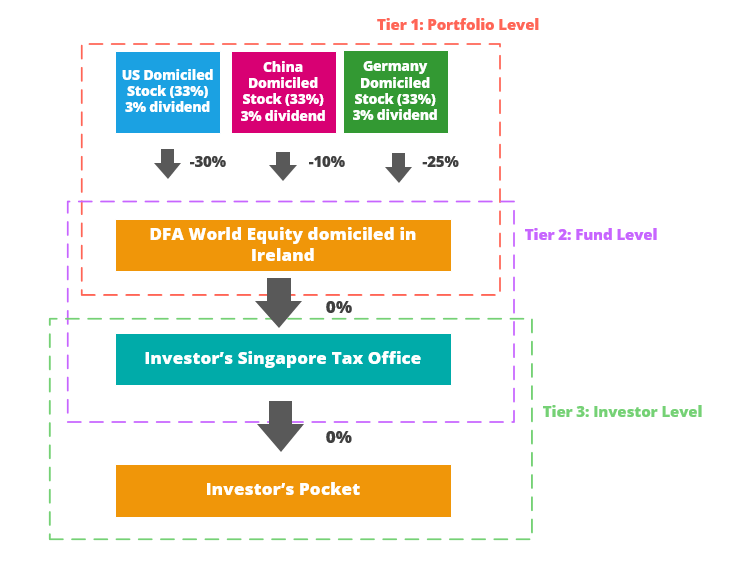

DFA World Equity Fund has higher expense ratio, wrapper fee, no forex risk, has 30% dividend withholding tax, no estate tax, dividend accumulating. Endowus has no platform fees, MoneyOwl is waiving it.

https://investmentmoats.com/money/invest-dimensional-fund-advisors-dfa-funds/

VT has lower expense ratio, forex risk, 30% dividend withholding tax, estate tax, dividend distributing, brokerage fees.

IWDA has lower expense ratio, forex risk, 15% dividend withholding tax, no estate tax, dividend accumulating, brokerage fees.

DFA World Equity Fund has higher expense ratio, wrapper fee, no forex risk, has 30% dividend withholding tax, no estate tax, dividend accumulating. Endowus has no platform fees, MoneyOwl is waiving it.

https://investmentmoats.com/money/invest-dimensional-fund-advisors-dfa-funds/

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

There are some problems with the spreadsheet, including:this article compares VT, IWDA, and DFA World Equity Fund. any thoughts?

1. Everybody has tracking error. There should be no zeros in that row. It's possible that a particular fund manager has more tracking error than some other, but if that's the case it'll be the gigantic fund managers like Vanguard and BlackRock that have the least.

2. Relatedly, there are bid-ask spreads with mutual funds and unit trusts, too. Part of the spread is incorporated in the lack of intra-day price quotations versus their exchange-traded counterparts. I really don't think there's any material difference here.

3. The U.S. estate tax rate is never 40%. It's always less than 40%, sometimes as low as zero. The 40% rate is only the top marginal U.S. estate tax rate, never the average rate.

4. I have no idea what the author means with a zero entry for dividend taxes in the Infinity Global column. Dividend taxes very much apply, always.

5. Some financial institutions charge dividend distribution and/or fund/corporate action fees, and I think that ought to be an additional row.

6. Some of these choices automatically reinvest dividends, and some don't. Automatic dividend reinvesting is usually more cost efficient.

VT, IWDA, and the DFA World Equity Fund have virtually the same forex risk(s), differing only in terms of the differences in the stocks they hold and their associated second order currency effects. DFA happens to be quoted in Singapore dollars, but that detail doesn't make any difference at all except that the fund manager handles the currency conversions to/from Singapore dollars on the buy/sell sides (since the vast majority of the securities the fund holds to track the global index are quoted/listed/traded in currencies other than Singapore dollars), and the currency conversion costs end up in the fund's total expense ratio (TER). Stocks are not currencies themselves, so there's no first order foreign currency risk when investing in stocks. Stocks are not bonds.

Last edited:

BBCWatcher

Arch-Supremacy Member

- Joined

- Jun 15, 2010

- Messages

- 23,018

- Reaction score

- 4,549

Business Insider noticed a fun fact: over half of Berkshire Hathaway’s market value now consists of Apple stock and cash. That high concentration risk might be OK, or even better than OK, for Warren Buffett — an open question, but maybe. However, you are not Warren Buffett with an investment company worth hundreds of billions of U.S. dollars. I don’t think your personal investment portfolio should be structured this way, and hopefully you’re not doing that.

Important Forum Advisory Note

This forum is moderated by volunteer moderators who will react only to members' feedback on posts. Moderators are not employees or representatives of HWZ. Forum members and moderators are responsible for their own posts.

Please refer to our Community Guidelines and Standards, Terms of Service and Member T&Cs for more information.

Please refer to our Community Guidelines and Standards, Terms of Service and Member T&Cs for more information.