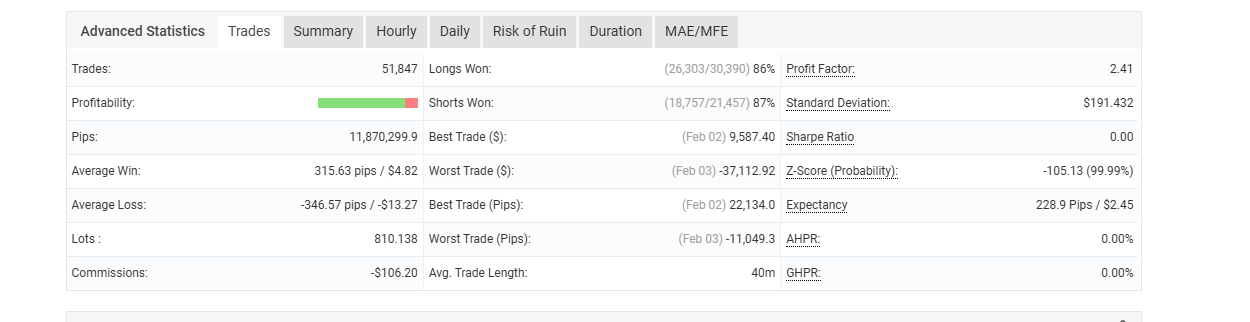

algo update done.

fixed a couple of gut feeling bugs, iterated through backtesting.

should be stable with no over runs on hedging.

hedging itself will be a revenue generation activity (once locked in hedge) and gap reducing (aka deleveraging) algo that works between the underwater longs and underwater shorts.

closing in on the gap with offset, so that the rebalancing (heding is always tilted) and with each bounce the higher side reduces.

eg.

xauusd long 0.08lots, short 0.10lots

heding rebalance +0.01 to long = 0.09 lots to short 0.10

when chart bounces down L = 0.09, short = 0.07. short rebalances to 0.08

lorum ipsum chart bounces up L = 0.05, short = 0.08, L topup to 0.07.

as you would realize with each bounce, the hedge side becomes the bigger lot, and overall reducing activity.

only complaint doing it on cny day 1

or read the chatgpt explaination below

Full Update: Hedge Compression Engine + Background

Several people asked whether this system is something famous traders use, and how it actually fits into broader trading theory.

Let me answer that properly.

First — no, you won’t find a well-known discretionary “guru” publicly teaching this exact structure.

However, the principles behind it are not new.

What this system combines are ideas that have existed in professional trading for decades:

- Market-neutral hedging

- Mean reversion / spread compression

- Volatility harvesting

- Inventory rebalancing (market maker style)

- Statistical convergence

Many institutional desks operate on similar mechanics — just expressed differently.

Market makers constantly rebalance inventory around a midpoint.

Stat-arb desks trade convergence between spreads.

Delta-neutral options traders rebalance to harvest gamma.

Some prop desks run structured grid or compression models inside defined ranges.

The difference here is implementation:

This structure applies symmetric hedge compression between underwater averages in a retail FX/CFD environment with residual tilt logic and inside-gap engagement.

So it’s not a “new theory.”

It’s a structured application of known mechanics.

How It Works Conceptually

Once both longs and shorts exist at different underwater averages, there is a defined price band between them.

Inside that band, price oscillates.

The system:

- Rebalances the smaller side toward the larger side.

- Always leaves a small residual difference (e.g., 0.01 lot).

- Places the first rebalance slightly inside the gap (5 pips offset).

This creates an inward bias.

Each oscillation:

- Reduces the temporarily dominant side.

- Tops up the smaller side.

- Gradually compresses imbalance.

Over time, if price remains bounded and continues oscillating, the imbalance trends toward the residual.

In theory, under continued bounded oscillation, imbalance converges:

If Dₙ is imbalance at cycle n,

then Dₙ₊₁ < Dₙ,

approaching the residual r.

In practical terms:

Repeated mean reversion + asymmetric rebalance = contraction.

That’s the compression engine.

Does It Outperform the Locked Unrealized?

Under oscillating conditions, it can.

Because:

- Realized gains accumulate on each reduction of the dominant side.

- The underwater gap tightens.

- Net exposure shrinks.

If volatility continues without runaway trend, the structure can eventually compress to near-flat and resolve itself.

However — and this is important —

If price trends aggressively without oscillation:

- Compression pauses.

- The hedge remains locked.

- Revenue generation slows.

This is not a magic drawdown eraser.

It is a structured volatility-harvesting system.

Why You Don’t See Famous Traders Publicly Using This

There are reasons:

- It requires strict risk control.

- It performs best in oscillating markets.

- Without capital discipline, grid-style compression can become dangerous.

- It is operationally complex.

Professional implementations usually layer on:

- Volatility filters

- Regime detection

- Position caps

- Capital allocation logic

- Dynamic exposure scaling

Without those, any compression model can fail under extreme trend conditions.

Final Thoughts

This approach is closer to how a market maker thinks than how a directional trader thinks.

It assumes markets oscillate more than they trend.

It works the range rather than predicting breakout.

It compresses rather than chases.

Is it famous?

No.

Is it structurally grounded in professional trading mechanics?

Yes.

Still refining, still testing, but mathematically and structurally it now behaves as intended.

And yes — most of this stabilization work happened on CNY Day 1

")