lifeafter41

High Supremacy Member

- Joined

- Oct 29, 2016

- Messages

- 28,753

- Reaction score

- 11,717

actually the large difference is not due compound interest. it is due to the pmt of 900 every year(+1% +1%)

10 years have 10 x 900 = 9000

120 months have 120 x 900 = 108000

difference already 100k without interest

cpf only compounds your interest yearly and not monthly

before i claim anymore credit, i would like to say that this method of calculation was taught by yywin.

I see dork......

The +1%, +1% gives the 900 max, understand now.

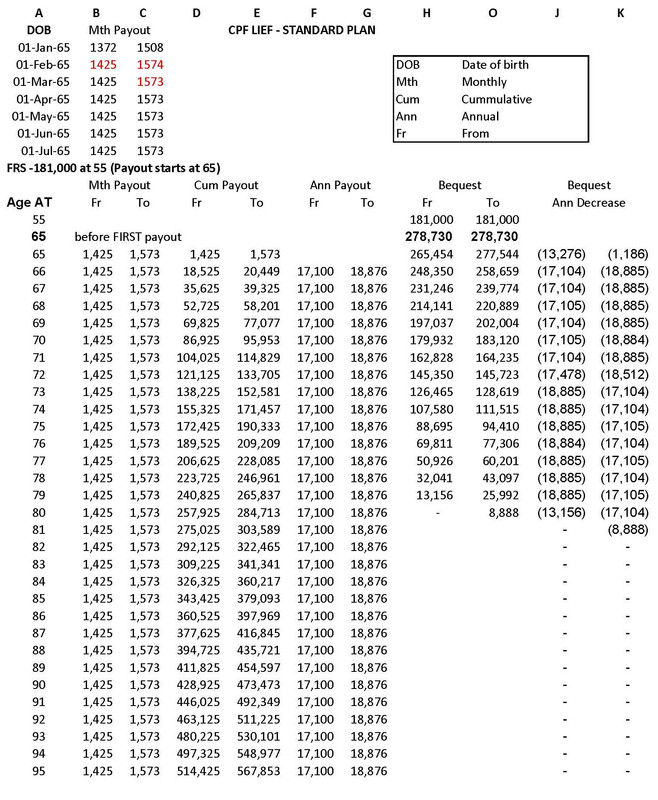

Is there aNother formulation to include a yearly top up to prevailing FRS or even ERS?

It’s just to see what’s the overall annuity insurance that’s going to be deducted when one reaches 65.