Hoe many % do you foresee can hit 90 and above?

straits times yesterday if you make it 65, chances of making to 90 is 1 in 3

Hoe many % do you foresee can hit 90 and above?

the higher irr is because basic earns interest and standard do not.

One is a function of the other.

The higher bequest with Basic is just a function of the interest earned on principle held back from pool participation.

You can’t touch this interest earned, but your loved ones might, IF you don’t outlive it.

The only thing anyone can touch with all 3 plans is “a payment” and a “possible bequest”... nothing more.

And since Basic has a lower payment than Standard, you alone cannot realize a higher IRR with Basic during your life, but collectively you and your family can.

Standard Plan for those turning 55 this year.

[/url]

It is earning 4%pa interest, read CPFB website, and read what I wrote about guaranteed vs non-guaranteed.

Maybe pool and non-pool balances earn 4%?

But for CPFL participants, longer living participants realize a higher % and shorter living participants realize a lower %. Those with a lower balance (BRS) also realize a higher %.

Maybe it averages out to 4% for everyone?

Why does it matter? Regardless of the inner workings, all you are going to get in the end are payments and a possible bequest.

One is a function of the other.

The higher bequest with Basic is just a function of the interest earned on principle held back from pool participation.

You can’t touch this interest earned, but your loved ones might, IF you don’t outlive it.

The only thing anyone can touch with all 3 plans is “a payment” and a “possible bequest”... nothing more.

And since Basic has a lower payment than Standard, you alone cannot realize a higher IRR with Basic during your life, but collectively you and your family can.

straits times yesterday if you make it 65, chances of making to 90 is 1 in 3

I'm a lay person. Can give based on %?

you wrote as though you do not understand the maths behind irr.

for cpf you draw down your own money. when you do that, irr does not change. it is the interest that the principal earns that determines the irr.

eg i have 200k in my ra under standard and the payout is 20000 a year, vs

i have 200k in my standard and the payout is 40000 a year.

the irr is 0 for both cases, as long as there is still money left in the annuity.

of course i will choose the one with 40k coz it will continue to pay if it hits 0

If CPF members alive today have the same mortality experience as past Singapore residents (this assumption is too pessimistic), then according to Singapore's 2019 life tables:Hoe many % do you foresee can hit 90 and above?

For Basic, you start with the same outflow, (regardless whether pooled or not) and add the inflows consisting of lower payments and final bequest payment (which will be higher, if you don’t outlive it).

I agree, if you only get back what you put in, the IRR is 0%. That is what happens with Standard & Escalating for about the first 15 years or so. Once the principle is exhausted and payments continue, you then start to see a positive IRR on the original amount invested.

To calculate the IRR all you need is the outflow (the original investment in the annuity) together with the inflows (annual payments and final bequest payment).

For Basic, you start with the same outflow, (regardless whether pooled or not) and add the inflows consisting of lower payments and final bequest payment (which will be higher, if you don’t outlive it).

Where the pooled versus non-pooled money goes, or how much interest it earns... doesn’t matter unless you (or your family) get your (their) hands on it via payments and/or bequest. Am I wrong?

if you are on rss, irr very easy to calculate. irr is 4%. this is because this was the interest of the RA.

Like i said, in flow, out flow not important in calculating

but cpf must come up with such a complex scheme, which makes the interest difficult to calculate.

eg

base 4%

+900 (+1%+1%)

-20% donated to annuity.

inflow only becomes important when there is no money left.

the calculation of the return based on FRS standard plan lowest amount(guaranteed) of 1350. not very accurate cause looking at annual payout instead of monthly and I didn't add the bequest amount before 80. but after 80, this is what u get.

the calculation of the return based on FRS standard plan lowest amount(guaranteed) of 1350. not very accurate cause looking at annual payout instead of monthly and I didn't add the bequest amount before 80. but after 80, this is what u get.

not like this meh??

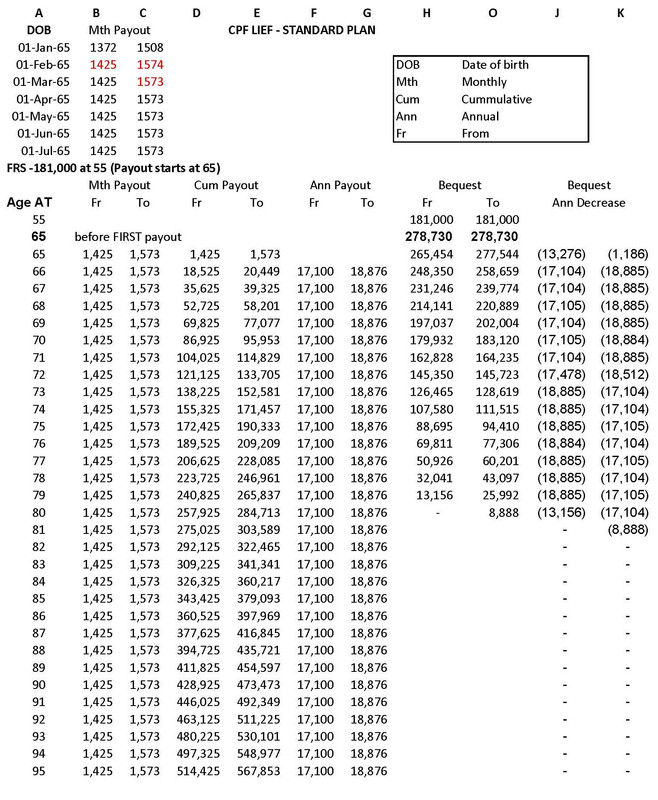

First thing, you need to add the interest earned from age 55-65. Currently for RA, that will generally be 6% on the first $30k, 5% on the next $30k and 4% on the rest. That would bring the $181,000 up to $278,730 for the annuity at age 65. If you want confirmation of this, look at the bequest chart from CPF, you will see at age 65 it is not $181k but between $250-300k.

Next, for Standard, the bequest each year is equal to the invested amount less any payments made. In other words, payments+bequest will be equal what you put in, or 0% IRR (until exhausted).

I would estimate payments of $1,430 or $17,160 per year in this scenario (because of the higher interest in RA earlier). That means the bequest runs out right after you turn 80 (same as the bequest chart shows) and after that the IRR% should be roughly 2.5% by 86, 3.1% by 88, 3.6% by 90, 4% by 92 and 4.5% by 95.

not like this meh??