1) Money market is cash equivalent... cash have no place in a portfolio.

when we talk about portfolio management, we do it in its entirety aka looking at all the different assest classes. Your protection assest (aka Term or WL) is considered part of portfolio. It is not just your investment tools that is your portfolio

Cash equivalents are for emergency fund not investment portfolio. Unless you are a retiree with a 80% bond portfolio then maybe 10-20% cash is warranted.

2) Fixed income is the bond fund... did you miss it?

Read below

3) Real estate in the form of REITs... yes it has been shown that it is a good class to diversify. However, I would not consider it a "core" asset class... something good to have but not necessary. This is why I left it out.

Real Estate may not be just in the form of REITs but also in a real assest form of physical real estate, resulting in passive income. Why leave it out when it serves to augment the portfolio?

Because the typical person does not have enough money to hold real physical property in a portfolio. Given a small condo can be worth 500k and a 10% allocation to REIT/property, this means that the net worth the investor must be 5 MIL. For those with only 500k, investing all the money in property is stupid because of the lack of diversification.

4) Gold/commodities is a grey area. First, there are conflicting studies on whether or not such asset class makes a good diversifier. Traditionally, they have had low correlation with other asset class, but in recent years that has not been the case due to speculators driving the commodity market. Secondly, the contango problems has made it impossible to invest in this asset class properly, because spot price cannot be tracked well. If you are familar with such things, then you will understand. Thus, I am ambivalent to this asset.

With the gold rush in the last 3-5 years, I agree with you that gold is rather speculative rather than a real demand. However as a real assest, Gold will serve to be a good asset class in the long run, since we are talking about a long-term portfolio, aren't we?[/quote]

If you want to talk about gold, one thing that we can conclude is that the role gold plays in many studies is that it smooths the long-term volatility but does not significant improve long-term expected performance. Gold has close to zero real return. That is why I said it is not essential. Good to have but not necessary, since with long time horizon, portfolio volatility is less of a concern.

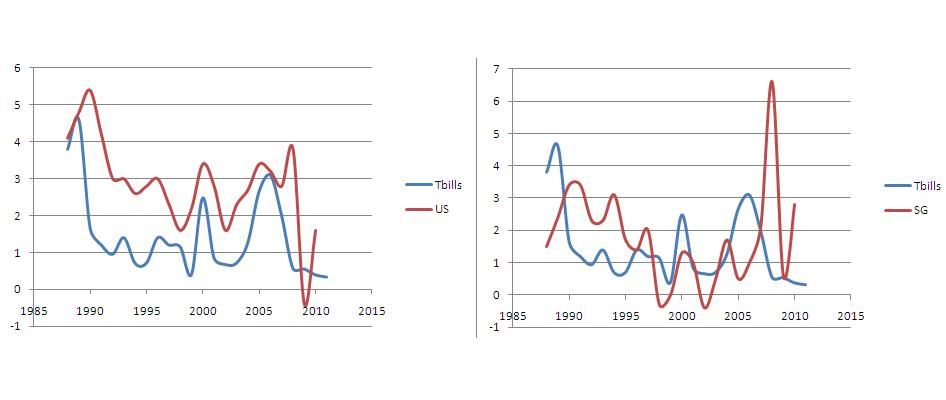

6) I am ambivalent to global bonds because there is the FX risk. The purpose of bonds is steady returns, why take on additional FX risk? We are not sure if the interest premium of global bonds will pay off in the long term vs local bonds. Again, it is a "good to have" but not a "core" asset class.

7) Emerging and High-Yield bonds, also known as junk bonds to me have no place in asset allocation. They may have higher yields but have equity like performance. So they are neither behave like normal bonds or stocks... not here nor there. What purpose would they serve in a portfolio?

Well your emerging bonds in recent years have seen a similar defaut risk as your investment grade bonds but however giving a much better yield due to the increased stability which shows my point that investment is something that continually evolves and needs adaptation.

You will need to cite your evidence that junk bonds have the same default risk as investment grade bonds. The very definition of junk bonds is INCREASED default risk.

Why is there no academic research to show for it now is because academics are often behind the curve. Why I have no sure-fire way to prove what I say. History has shown time and again that academic research is not the Gospel truth.

Again your strawman attack on the self-correcting nature of research. I won't entertain you any further.

If passive investing is the BEST method, then why the continual debate about it versus active investing in the academic front as well? Reason is that THERE IS ALSO NO CONCLUSIVE EVIDENCE TO PROVE that one is more superior than the other.

If given a fact that one with LITTLE TIME, inability to digest vast information, YES then I agree with you that by investing into index funds is probably a much better choice. It gives you the BEST average returns BUT that doesn't mean active investing is inferior.

Continued debate in the finance industry is because they have a vested interest to charge high management fee for a non-existent value-added service of beating the market. Continued research in the academic front is to expand the horizons of knowledge, maybe one day there will be method that can beat the method but IT DOES NOT EXIST today. The burden of proof is on active investors to provide a methodology and show that it works at a statistically significant level.

As you have admitted as well, there ARE funds/people/managers who CONSISTENTLY BEAT the index OVER AN EXTENDED TIME. You are merely in your comfort zone because you FEEL SINCE THERE IS NO CONCLUSIVE EVIDENCE/PROOF, I shall stick to index. Pretty much of your kiasee mentality as well? No?

Personal attacks are boring, shows your emptyness. It is not a feeling that there is no conclusive evidence/proof, IT IS A FACT. Coin toss is always a good investment analogy. If a predict coin tosses correctly 1000X in a row, am I lucky or skillful?