I’ve explained exactly what my spouse and I do/did previously, but here’s the summary. We both piled into CPF MA and SA quickly upon becoming CPF members since we didn’t have the head start most of you had. That means/meant:

* Full OA to SA transfers every month;

* MA top-ups with whatever room was left to the CPF Annual Limit, up to the Basic Healthcare Sum;

* $7,000 SA top-ups every year.

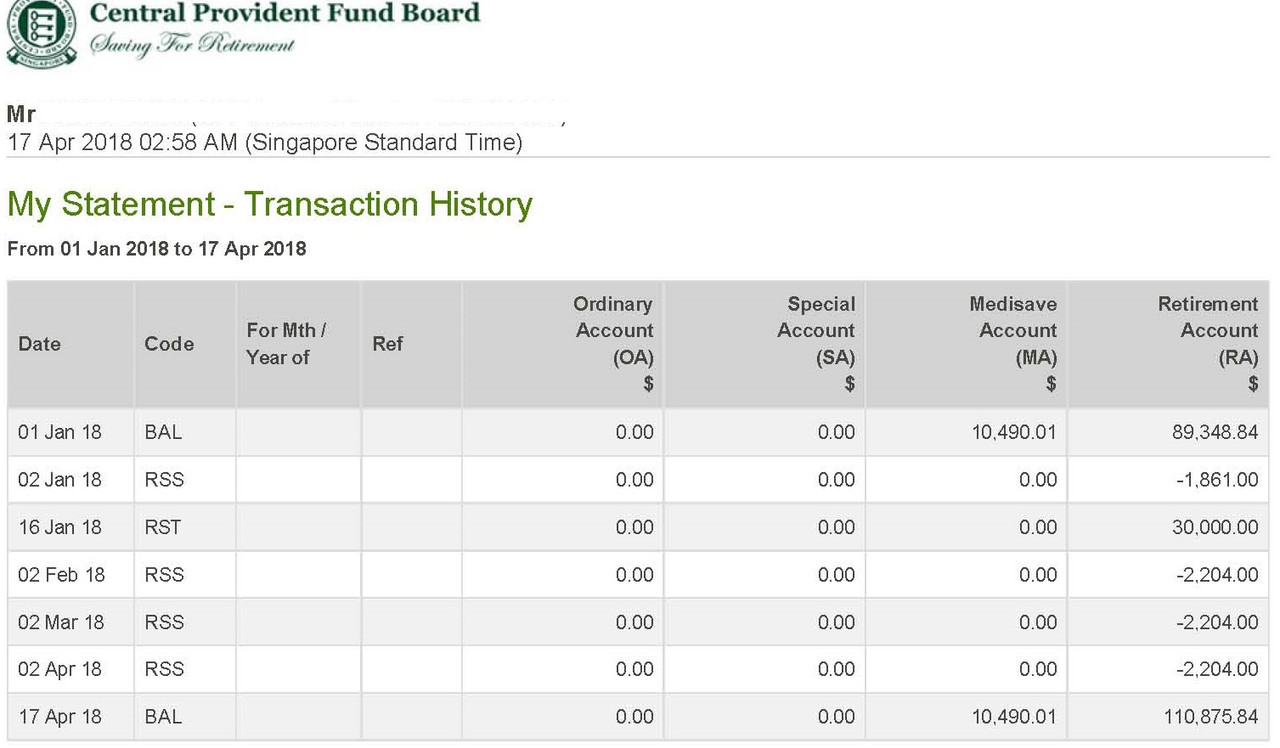

With that particular recipe you max out bonus interest pretty quickly then sail past the 6 figure mark not much longer after that. That’s because you’re pushing in $47,740 each calendar year (the $37,740 CPF Annual Limit which ends up all in MA and SA, and another $7,000 in SA), including the partial year you first become a CPF member. Add the 4% and some bonus interest to that flow, and only modest MA withdrawals for hospitalization insurance, and the total balances rocket up pretty quickly. And there’s tax relief, too. I think my spouse aimed a little under the $47,740 figure since the tax relief worked a little better that way, but it wasn’t a much smaller rocket.

This approach is viable and best for us, in our particular circumstances.

He is such a good role-model

He is such a good role-model

")