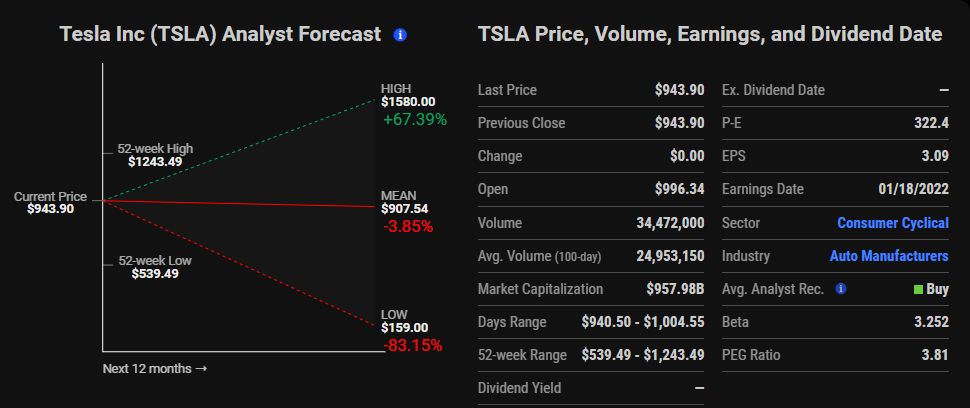

Tesla earnings to be announced this Wed. If earnings soar, it might be the only high-cap tech stock huating for this week to lead the charge. But if they miss earnings.....Not for the faint-hearted, LOL.

https://ir.tesla.com/press-release/...-full-year-2021-financial-results-and-webcast

AUSTIN, Texas, January 12, 2022 – Tesla will post its financial results for the fourth quarter and full year ended December 31, 2021 after market close on Wednesday, January 26, 2022. At that time, Tesla will issue a brief advisory containing a link to the Q4 and full year 2021 update, which will be available on Tesla’s Investor Relations website. Tesla management will hold a live question and answer webcast that day at 4:30 p.m. Central Time (5:30 p.m. Eastern Time) to discuss the Company’s financial and business results and outlook.

What: Date of Tesla Q4 and full year 2021 Financial Results and Q&A Webcast

When: Wednesday, January 26, 2022

Time: 4:30 p.m. Central Time / 5:30 p.m. Eastern Time

Q4 & FY 2021 Update:

http://ir.tesla.com

Webcast:

http://ir.tesla.com (live and replay)

Approximately two hours after the Q&A session, an archived version of the webcast will be available on the Company’s website.

For additional information, please visit

http://ir.tesla.com.

------------------