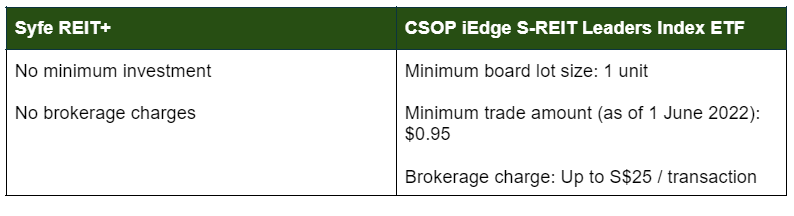

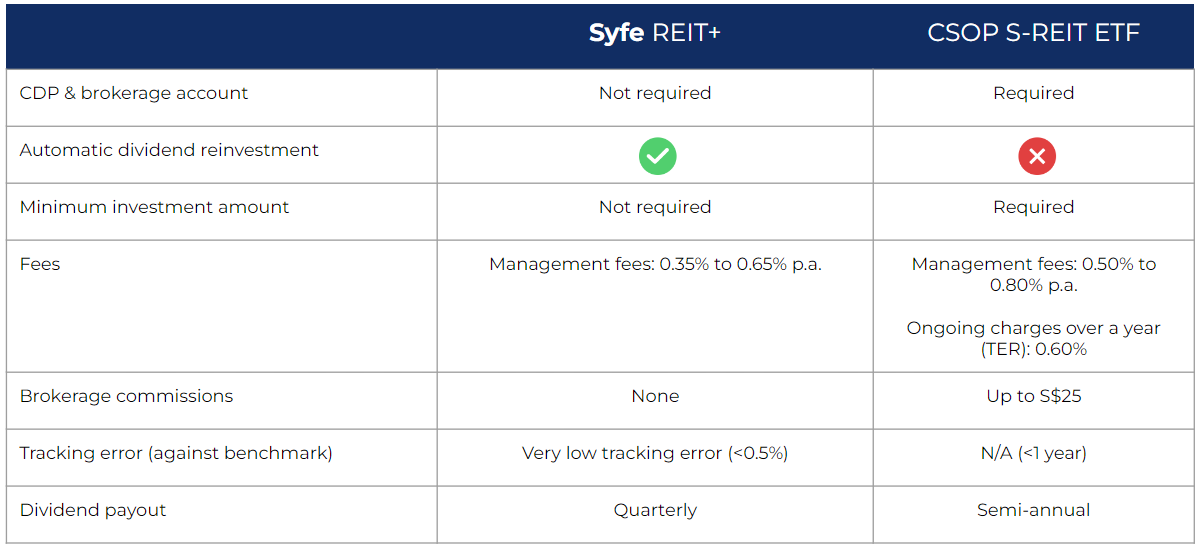

i hope no1 gave up Syfe Reits by now, i m still holding it for Parents (and myself for comparison)

https://www.syfe.com/magazine/singapore-reits-whats-ahead-for-2022/

S-REITs in Rising Rates

REITs, along with other capital intensive sectors, are sensitive to interest rates, given their impact on borrowing costs and yield spreads. To mitigate the downside risks, S-REITs have been

managing their interest rate exposures actively. According to SGX, on average, close to 75% of S-REITs’ current debts are either in fixed rates or hedged through floating-to-fixed interest rate swaps.

In addition, S-REITs currently have an average gearing ratio of 37%, comfortably below the regulatory threshold of 50%. Gearing ratio, which measures leverage, is calculated by dividing total borrowings by total assets. A lower gearing ratio below the threshold implies healthy balance sheets and that S-REITs can service their debt and still have room to raise more debt (if and when needed) for additional acquisitions or operations.

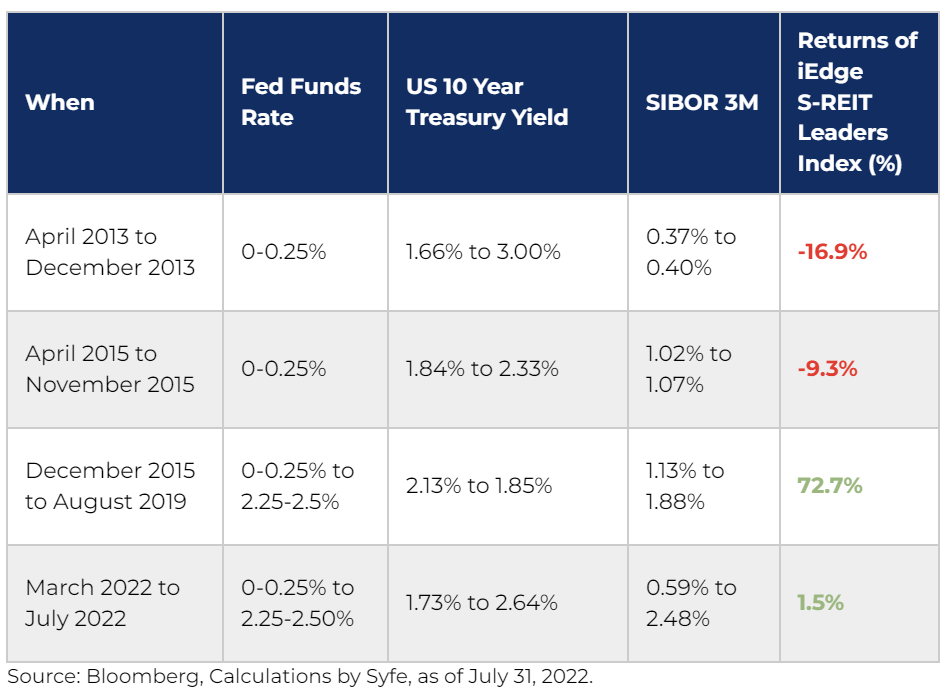

Looking at periods in the past where the Fed funds rate has increased along with the 3m SIBOR rate, performance of S-REITs have been mixed.

During the taper tantrum of 2013, S-REITs fell by close to 17% over 9 months. In 2015, where global markets experienced a sell-off with the Greek debt default, a sharp fall in petroleum prices, and slowing growth in China, S-REITs fell 9% over 8 months.

However, from the time we saw the first rate hike in late 2015 to when the Fed funds rate hit 2.25-2.5% (the highest in ten years), S-REITs delivered stellar performance of almost 73%.

So far this year,

S-REITs have remained relatively defensive after the Federal Reserve increased interest rate nine notches (once in March, two notches in May and three notches in June and July). For the first six months of 2022, while global equities (as measured by MSCI World index) fell close to 20%, S-REITs are down 2.9%. Despite the large hike in July, S-REITs gained 3%.

But what if we are heading towards stagflation or recession?

The effects of higher inflation are difficult to ignore. Along with global central banks, the Monetary Authority of Singapore (MAS)has tightened monetary policy to rein in inflation. The labor market remains

robust (unemployment rate of 2.9% and 242 job openings for every 100 unemployed persons), and domestic and global economic growth is still expected to be

positive. MTI stated earlier in July that Singapore does not expect its economy to slide into a recession or stagnation in 2023, despite global headwinds.

We looked at how S-REITs have done when Singapore’s GDP has grown or contracted over the last 10 years.

Perhaps surprisingly, REITs tend to have moderately positive returns when the economy grows at 2-5%, and grow more in periods of lower growth than in periods of higher growth. As this year’s forecast is expected to fall between 3-5%, even if growth comes in slightly under target, S-REITs could still be in a good spot – a bit like Goldilocks: just right!